We were almost ready to take the plunge and put a lot of dough into the Vanguard All-World ETF at a 0.25% TER…when I started investigating the dividend leakage. I was triggered by Meesman’s article. This thing causes some serious damage to your investments placed outside of your home country. This is because the other country’s government charges a very scary thing called dividend tax. It’s illegal, it’s unfair and it’s a financial independence killer. Just read this. Yikes!

This dividend tax leakage especially hurts ETFs and index funds. This leads to an unrecoverable tracking error between the fund and its index benchmark! These European investment vehicles underperform their benchmarks by 50 to 150 basis points per year. That’s a significant cost for investors! According to the fore mentioned article the extent of tax leakage varies widely by index type. However, tax leakage represents a GREATER COST to investors than expense ratios! This is the worst possible outcome…obviously.

As Vanguard is domiciled in Ireland a Dutch investor (or any European investor not from Ireland) is charged dividend tax by the Irish government. Whereas the Irish investor can claim this dividend tax back from the government, the rest of us Europeans can’t. And we can’t claim anything on our own government either. We don’t even get to see the real dividend. We’ll receive 85% of the total dividend, and that’s that. The Irish government will already have taken its (NOT so fair) share. That comes down to adding 0.4%-0.6% to your TER. So our Vanguard All World ETF would intrinsically cost 0.65%-0.85% instead of the 0.25% we were promised. 😦

Yeah, it’s illegal and unfair. The EU already stated in 2004 that dividend tax on individuals doesn’t comply with the EU treaty. The European Commission has already told all member states to stop this unfair practice. Even the European Court of Justice ruled that member states didn’t comply with the treaty multiple times, for example in this case against the UK in 2012. Multinationals have been fighting this injustice through the ECJ for almost a decade now. Every time the ECJ rules in their favour…but there’s not one member state that complies! They will lose millions in tax income. Experts think the turning point is almost there……but should we believe these fortune tellers?

Lo and behold, there’s a solution! A smart Dutch broker decided to act and created its very own FBI (Fiscale Beleggingsinstelling, it’s this fiscal arrangement so that the funds can now be domiciled in The Netherlands) in 2010. This year Meesman switched its Global Fund from Vanguard to accommodate it with Northern Trust making it the first MSCI World Index Fund without dividend tax leakage. This could make up for an extra 0.4 to 0.5 going to the investor per year. Yay! Problem solved! Let’s invest with ThinkCapital or Meesman! Whoohooo!

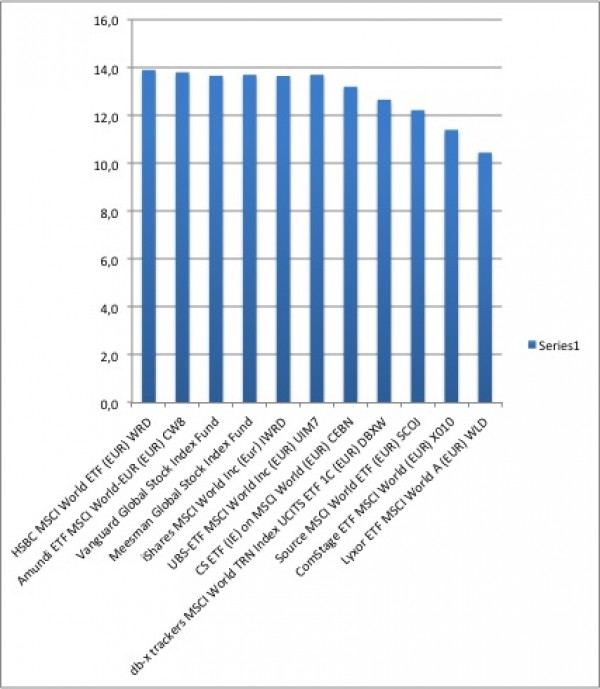

Hold your horses! Let’s get back to that MSCI World Index, now shall we? You’d think that any fund tracking that same index would have the same results, right? WRONG!

This shows the 2012 results for a couple of index funds and ETFs that track the same MSCI World index.

I nicked this graph from Ms. Verdegaal’s article which explains the situation in Dutch. She got it from Morningstar and Meesman.

A 3% difference between the best and worst performing fund! WTF?! This means you have to study all fund prospectuses. What are the costs? Is it expensive to get in and out? Who receives the dividend? How precisely does the tracker follow the index? Are you really buying stocks or just renting them? Do they rent out your stocks? If so, do you get paid rent for that service? This means you have to compare results yourself, for example, via Morningstar but that ain’t easy. Sigh!

It gets worse. I have already explained the transaction costs with Meesman will get ridiculous as soon as you want to invest or extract bigger amounts (€2.000+) and they don’t have a limit like BinckBank. However, the husband needs to calculate whether their solution to the dividend tax leakage makes up for that. Now, it’s difficult to compare because they used to invest with Vanguard (and performed really well, according to the graph!) but now with Northern Trust (I haven’t been able to find their performance in 2012 and compare that, if there’s a reader that does…?). With Vanguard they used to follow the MSCI Index very closely and you’d own a mix of all 1600 or so stocks in it. Which is what you’re after.

Okay, let’s look at ThinkCapital as well then. No dividend tax leakage either. Happy, happy, joy, joy! Oh, goody, they offer the Think Global Equity UCITS ETF and charge only 0.2% TER! Yes, yes, yes! Click! I want to get me some MSCI World Index funds without the dividend tax leakage, thank you! Since it’s in Dutch I’ll sort of translate….the Think Global Equity UCITS ETF is spread into 250 world-wide stocks and tracks the Think Global Equity Index. Eh? The results of this ETF can be COMPARED to the results of the MSCI World Index. Huh? What happened to the 1600+ stocks thingy? Where’s the diversification? Son of a ………! Oh, their own benchmark (which is NOT the MSCI World Index) in 2012 was 14.24% and their actual result was 13.59%.

Geographically you’d be investing in the U.S. (38.32%), Japan (18.56%), France (7.2%), the U.K. (7.26%), Germany (6.26%), Switzerland (4.15%), Australia (3.03%) and a bunch of other developed countries.

A huge difference with the Vanguard MSCI World Index where you’d be investing in the U.S. (53.61%), Canada (4.22%), the U.K. (9.12%), Western Europe “Euro” (12.09%), Western Europe “Non-Euro” (6.17%), Japan (9.25%) and a bit of other countries. No emerging either.

To me it looks like they’re fiddling around with their own benchmark and I have no idea whether this will turn out for the best. Tracking the complete MSCI World Index feels a lot better.

The other ETFs they offer we do not find interesting at all.

So, what’s a girl to do? Stick with Meesman and pray for the best? Dive into Vanguard and pray that member states will give up their sadistic dividend tax habits? Take a gamble and go for ThinkCapital?

Aaaaaaaarrrrrrrrgggggggghhhhhhhh! INDEX INVESTING IN EUROPE IS NOT EASY, I DON’T CARE WHO YOU ARE, IT JUST AIN’T!

Let’s move to the U.S. and invest with Vanguard directly! Yeah! 😉

Okay, stop being such a complainypants and look at the bright side. At least now you now more of what you’d be buying. Plus, you’re still much better off than investing with a managed fund because you’d still be way under 1% TER.

If you Dutchies are interested in a dividend tax leakage discussion, this is a good place to start. I will phone our tax services about our treaty with Ireland and the double taxation that now occurs. Ireland takes 15% and dividend is taxed 30% in The Netherlands. I’ll keep on investigating this very important matter…

What would you advise us to do? Anybody? Somebody?

Love,

Mrs EconoWiser

Disclaimer: I am not a professional investor nor do I claim to be one. You are solely responsible for your own financial and investment choices. I am not responsible for inaccurate information in any of my blog post. I am merely sharing ideas and findings of my very amateurish investigation in index investing.